The return of volatility

At the start of June, as a part of a hedging strategy, I purchased VIX call options. The call options would be a winning bet if volatility in the broader market increased.

This was a wager anticipating several factors at the time such as recent market performance (to the upside), a revised point of view on market valuation (expensive), the likelihood of upcoming Federal Reserve action, and, maybe most importantly, a relatively historic lack of volatility of late.

This trade was re-upped at the start of July. The VIX was around 12.00.

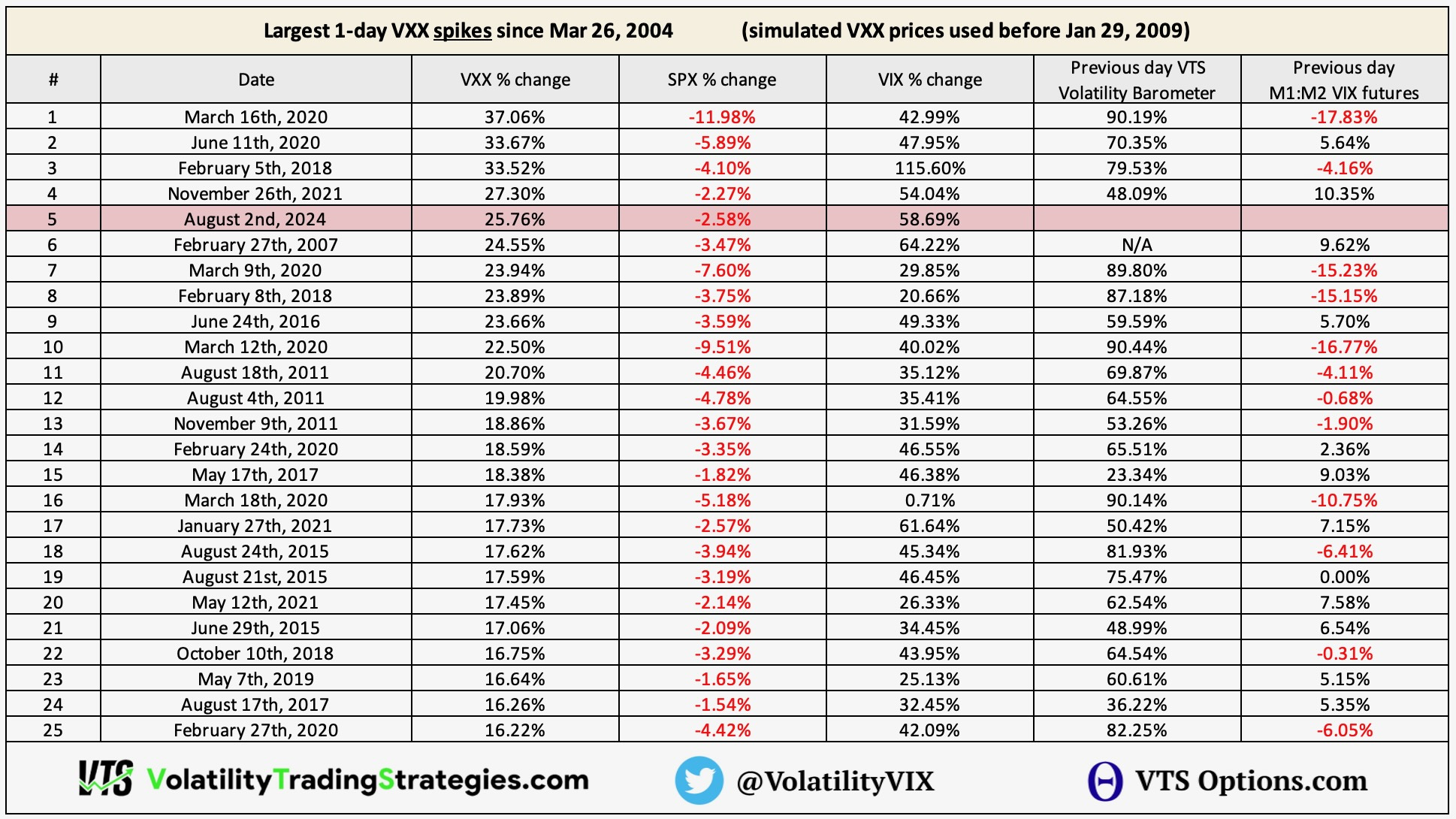

The past few weeks have seen a return of volatility, culminating in a large spike today.

It’s the highest level on the VIX since March 2023 during the regional banking chaos. Moreover, somewhat surprisingly, it looks like today was actually one of the largest VIX moves in history.