2025 Q3 Portfolio Update

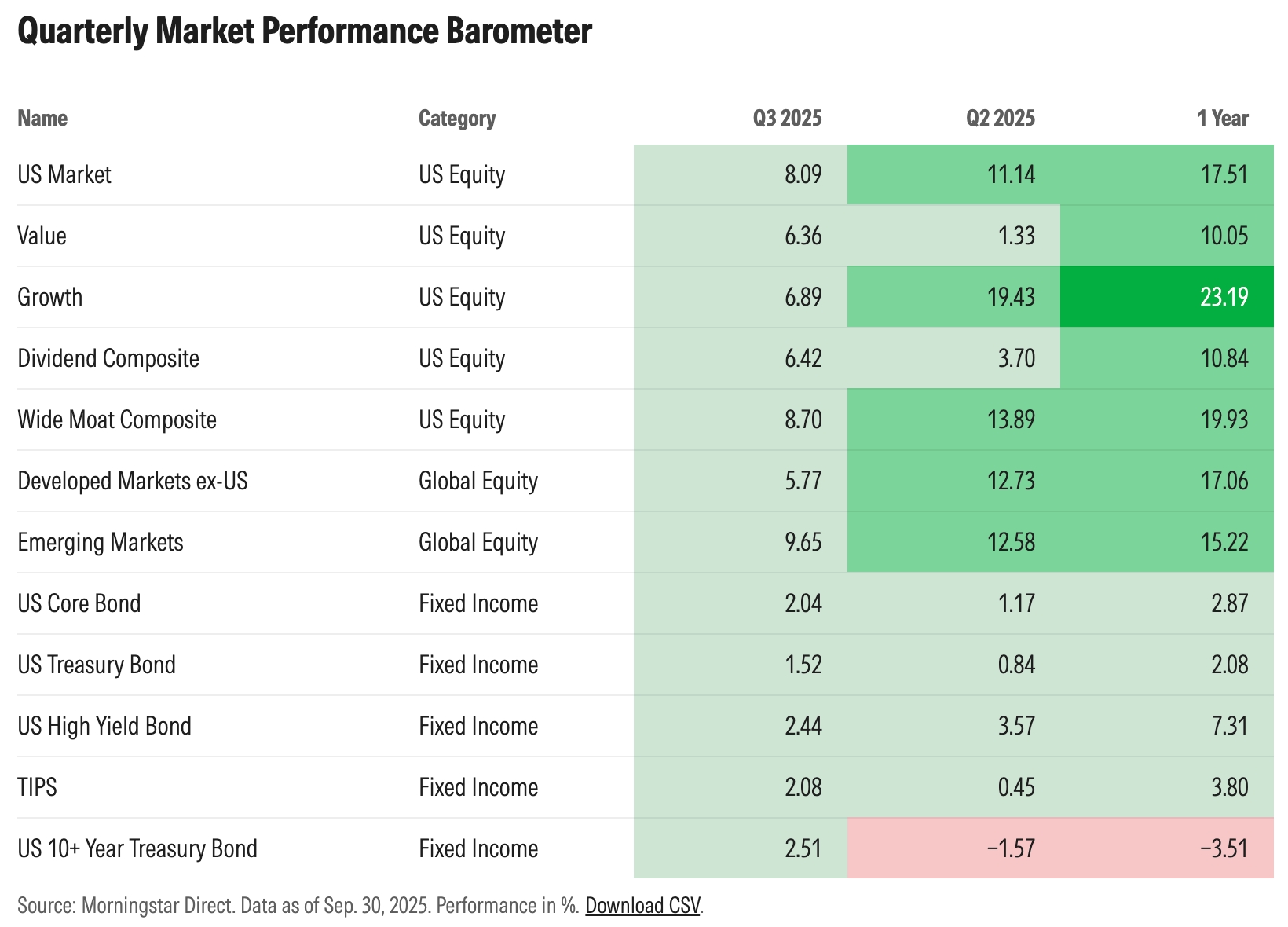

The third quarter of 2025 produced results in a much more homogeneous fashion than the relative chaos of the second quarter. Where Q2 had wild swings and varied performance by asset class, Q3 was more a steady march higher across assets.

Overall, the S&P 500 was up 8% in the quarter.

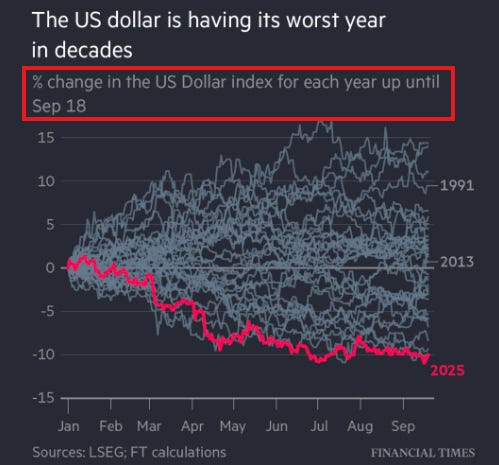

Everything is working with one very important exception —the U.S. dollar.

As I’ve bragged about multiple times (and importantly broadcasted at the end of 2024), we had a leveraged short on the dollar to start 2025. It literally could it have been better timed.

Outside of the dollar, it does feel like we are in “melt up” mode at this point. The thing is, this can last months or even years. And there are a number of reasons to think this will last.

The White House is cutting taxes.

The Fed is cutting rates.

There’s a beautiful bull market story around productivity via the large langue models and broader A.I. infrastructure build out.

Back to the dollar. No one wants to hold it, so flows continue to move to, well, anything but the dollar. That’s meant big flows into U.S. stocks, gold, and bitcoin.

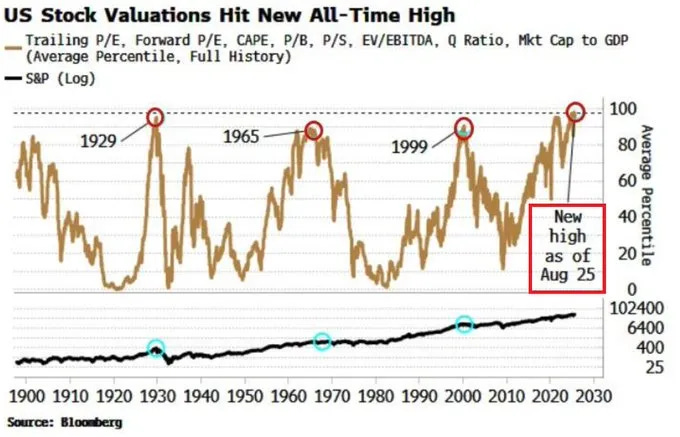

And these are the facts at a time when the stock market is at all time highs. This is clearly the time for the old saying, “All time highs beget new all time highs.” It is going to take something to stop the momentum.

Still, today I can find the scary data points. Like, right now. Nowadays this is mainly around valuation. And some are shared in our Q3 Chart, Graphs, and Tables Megapost. Here’s just one.

It’s a good one because it not only uses historical percentiles (instead of a raw number), but also looks at an average of eight different valuations metrics.

Prices today are rich.

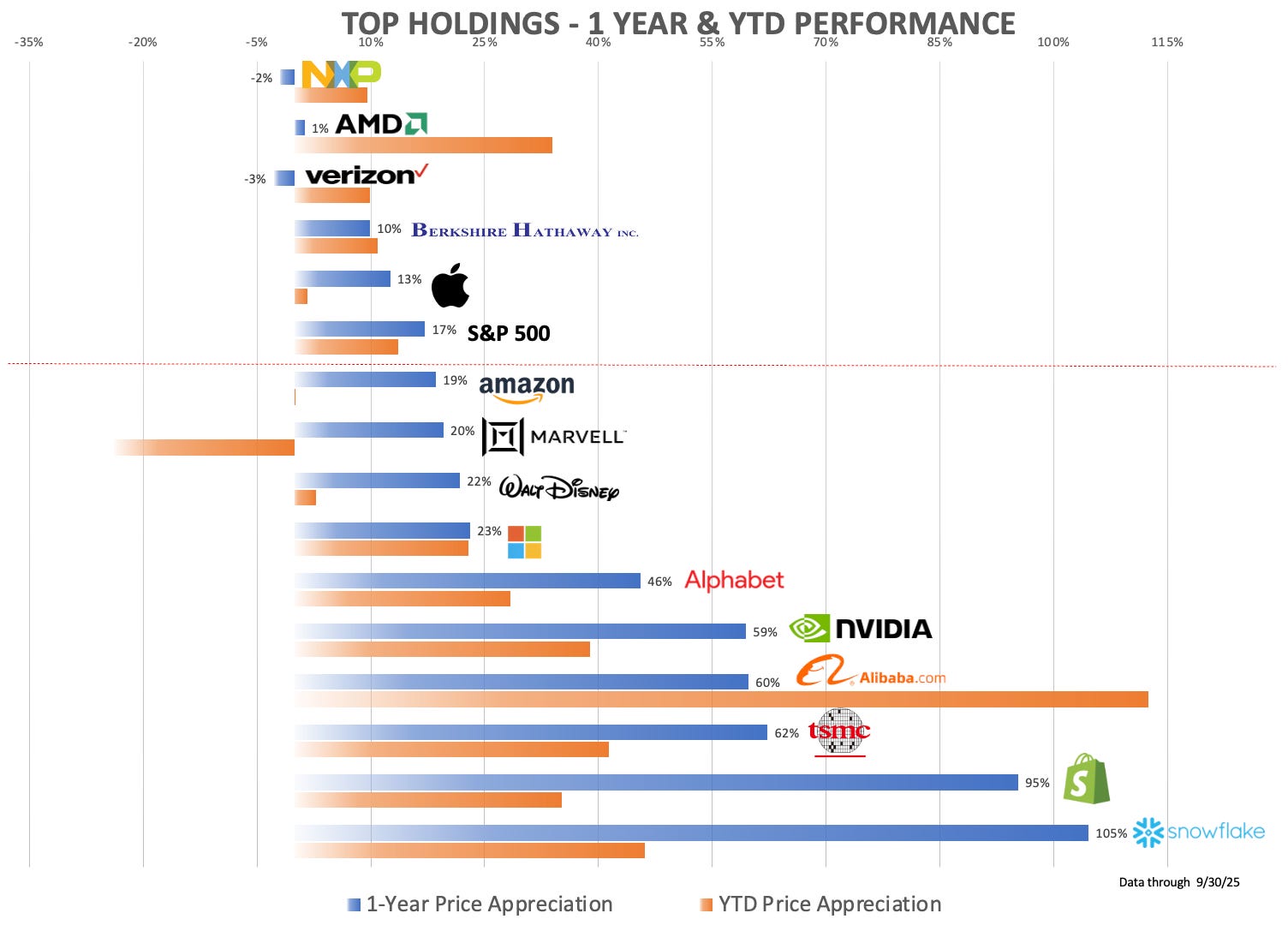

Top Holdings

Turning to the top holdings in the portfolio. Ten of our fifteen positions have outperformed the S&P 500 over the past year as of September 30th.

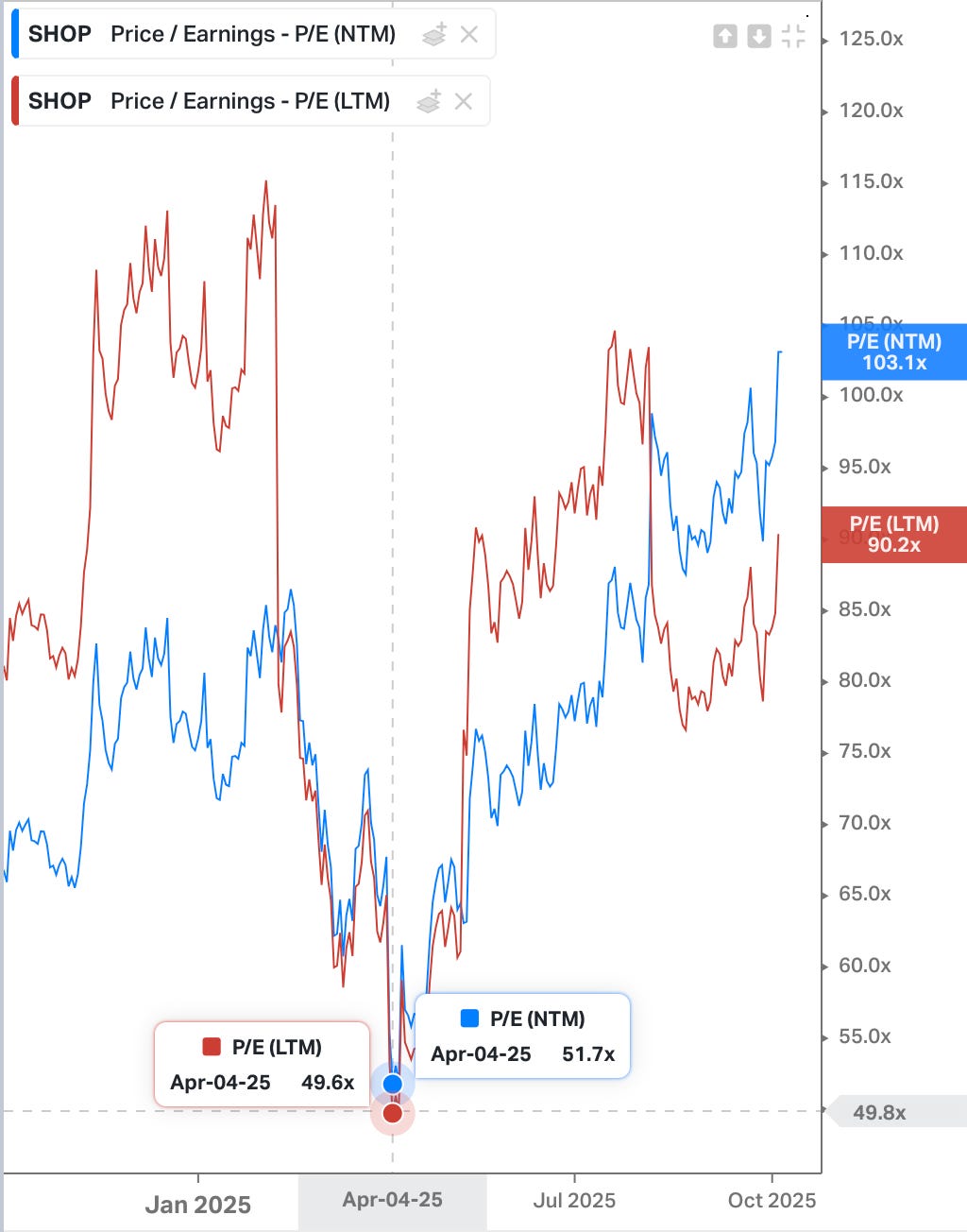

Regarding those pesky valuations, the riskier contingent of tech companies have basically become twice as expensive as a group since Liberation Day in April. Snowflake and Shopify are the clear examples among the top holdings.

All-in-all, it doesn’t seem reasonable, but I think that’s where we are in the current market cycle. Reason sometimes doesn’t matter in the short term. And the sentiment could have staying power, too, on the back of the very bullish bullets listed above.

Analog Boy

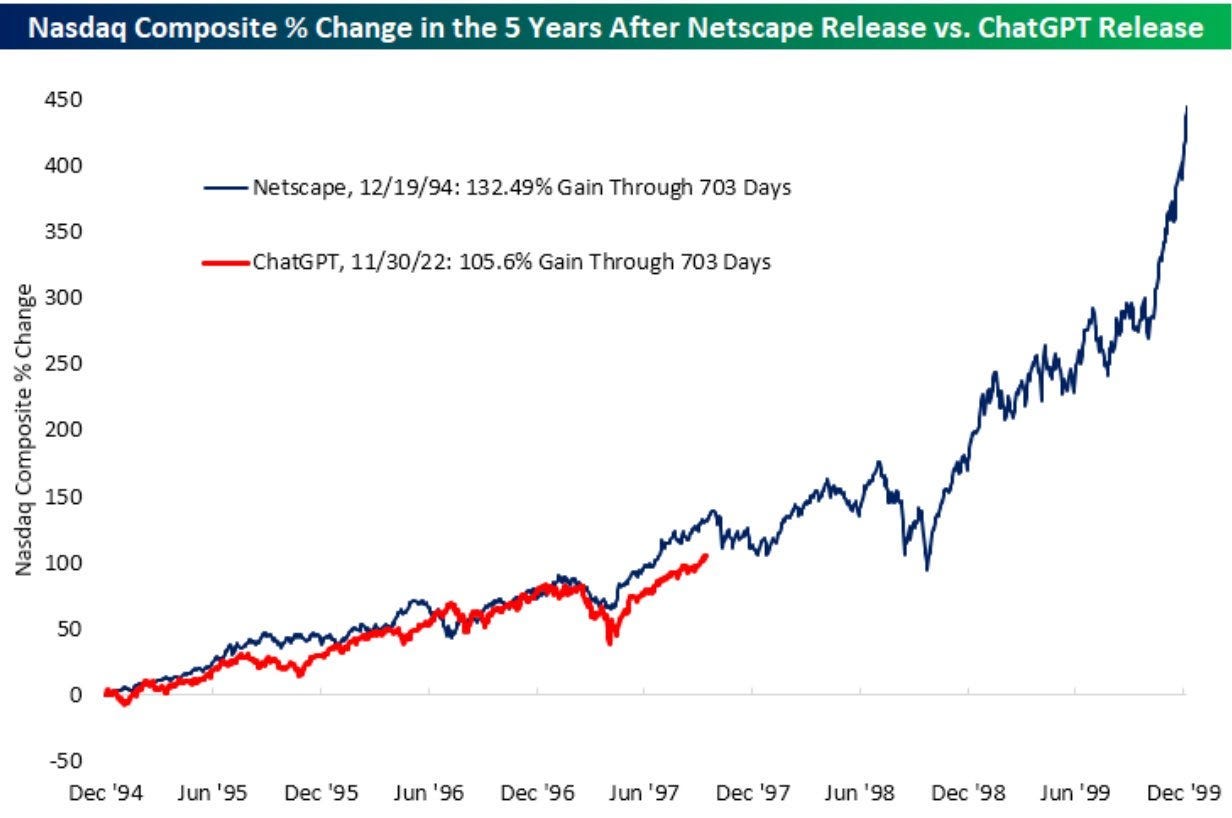

There’s various versions of this 1994 bull market analog going around.

I have a huge soft spot (but hopefully not blind spot) for a good market analog. This stems from the cult classic documentary Trader in which Paul Tudor Jones and Peter Borish appear to use an analog from the lead up to 1929 to predict 1987.1

While I don’t think analog markets are a panacea to allocate money, they are sometimes a reminder of how markets tend to move. Narrative is a big part of how markets move, and the “Internet is to ChatGPT” comparison is certainly a compelling narrative; “ChatGPT will be as big for productivity as the internet was.”2

The narrative is there for a confined bull market. But, at some point, the fundamentals matter. Today’s U.S. companies have, on average, significantly better margins than decades prior. Still, those margins are not flowing to the bottom line in a manner that supports current valuations.

If something even more substantive than the bullish bullets above does not come to fruition, valuations will get reset. It may take months, or more, but it will happen.

There was undoubtedly more to it. But the analog is one of the apex moments in the doc. Hollywood!

The interesting thing about using Netscape as the tracking stock is that Netscape ends up going away. It’s very much a minority opinion that OpenAI will not be at least the consumer winner in generative A.I.