More on volatility; hedging

As I wrote last Friday, the portfolio was long volatility as part of a hedge. An important addendum for context; I make only a handful of trades in a given year, on average. I am, overall, a longterm investor not a trader.1 For 2024, I put four trades out there at the start of the year. Three of the four have now hit with the fourth still an open possibility.2

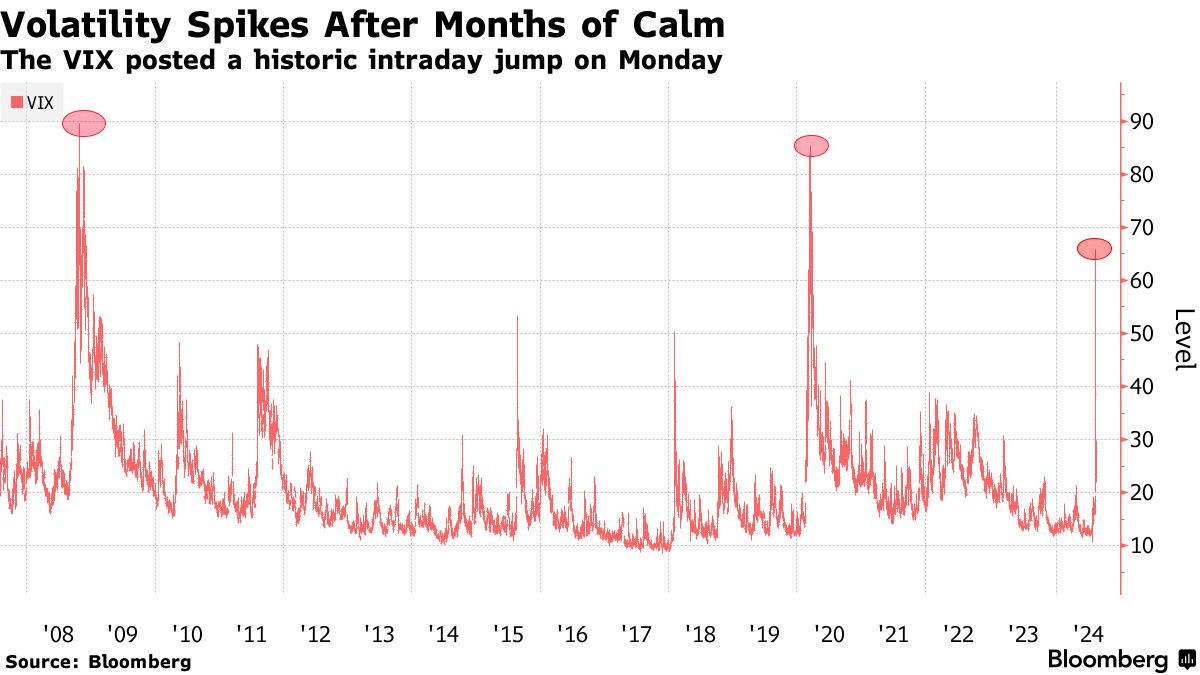

Back to volatility. Volatility can be measured by the VIX. Volatility had been muted since March 2020, but it was unusually low in recent weeks (hitting below a 12 reading on the VIX). The VIX was irrelevant, it seemed.3 Thus this was an extremely lonely trade when I went long in early June. And for that reason it was an extremely cheap trade when I re-initiated it on July 1.

Fast forwarding; there was a 60+ reading on the VIX on Monday morning.4

But what has created confusion is that most (if not all) of the traded products, which are built on VIX futures, did not hit that 60+ level. See chart below.

The VIX did spike. The VIX futures did spike, but not as much.5

The result in the market was an S&P 500 down nearly 6%, and the Nasdaq Composite down almost 8%, to start Monday morning.

Like most things, the reason behind this event was probably multifactorial. There is the carry trade, the dispersion trade, the unwinding of the short volatility trade, a jobs report, Buffet selling Apple, Kamala Harris edging towards becoming the presidential favorite, and more.

I read someone say, yes, there was “fear” on Monday. But it did not feel like there was “panic” on Monday. And many believe you need panic to serve as a “market clearing” type event that leads to sustainable new market highs. So, the interesting broader question is whether or not the brief selloff serves as such as event. If it did not, there could be more volatility to come.6

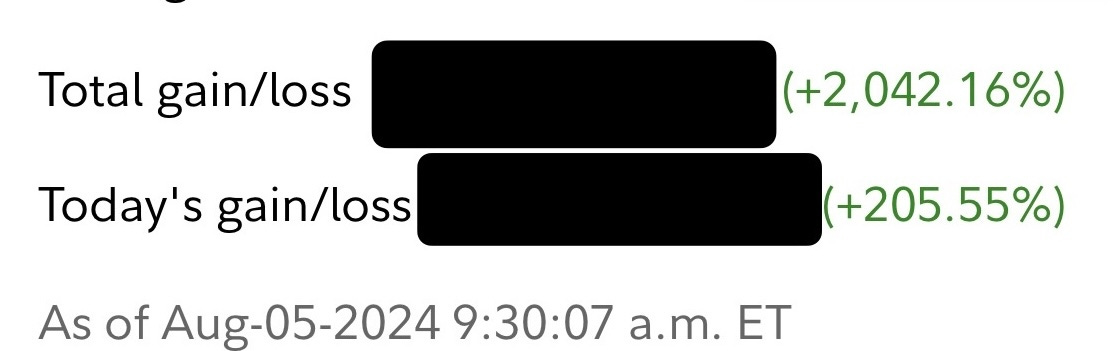

In the end, the trade ended up being 24x return in just over a 1 month period.7

Whether it was a 30-something reading or a 60+ reading on the VIX; not a dime back.

Hey, that’s the name of the blog!

Importantly, these are long to very long odd trades. One beat I’ve been on for awhile was (a) the lack of volatility, and (b) hedge funds getting short volatility. This, in part, is why this ended up being a portion of my hedge. Specifically, there was a good Odd Lots episode at the start of the year and other thoughtful pieces rightfully calling out the historic volatility lows. I’ve pulled in one such headline.

The remaining bet on a recession was made at extremely long odds. As the saying goes, the time to buy fire insurance is not when your house is on fire because the price will reflect the current risk.

In fact a popular hedge fund trade has been to short the VIX in various ways.

This is a sidebar as there was a lot of chatter about; (a) why there was such a difference, (b) how much of the volatility could be monetized through the traded products.

If I think about it now that I am beyond the fog of war associated with unloading my position, this very likely may not have been the type of selloff that paves the way for new highs. More likely, there is substantial risk to the downside in the short-term. Fear but not panic.

The screenshot is from the market open. I do feel fortunate that my brokerage was (mostly) working on Monday morning, while many weren’t, and I was able to get out of my position at damn near the top.